We have broken down the real estate sales market for Grenada for quarter 1 to quarter 2 of 2025 and made comparisons with 2024 sales within the same period to examine the market performance.

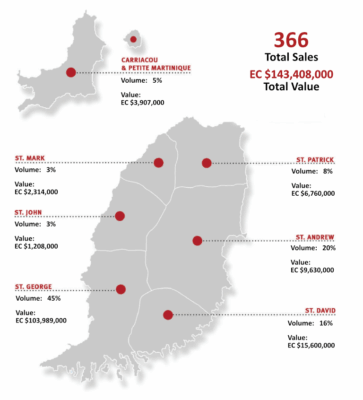

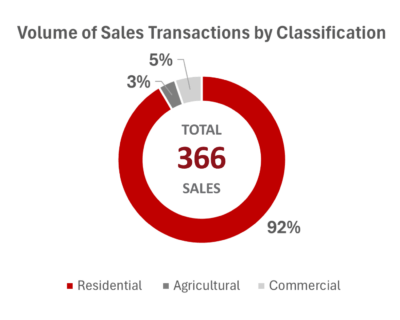

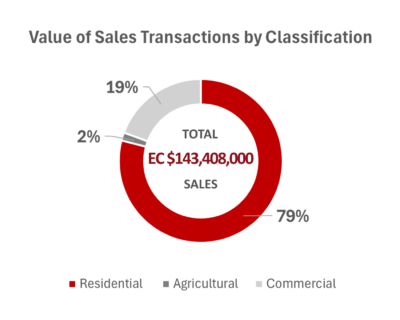

Grenada’s real estate market trends remained fairly stable through the first half of 2025. A total of 366 transactions were recorded, amounting to approximately EC $143.4 million.

![]()

• 366 sale transactions were registered for Q1-Q2 of 2025

• The total volume of sales remained fairly stable compared to Q1-Q2 of 2024

![]()

- Total value of sale transactions registered – EC $143,400,000 (rd) for Q1-Q2 of 2025

- There was a decline in the total value of sales in Q1 of 2025 when compared to 2024 for the same period (2024 Q1), while stable in the second quarter.

- The decline in total value is a result of two large sales within Q1 of 2024.

NOTE: Transactions like these (primarily large development sites) are significantly higher in value, thereby increasing the overall performance of any given year or quarter. In some cases, the sale of one development site can be greater in value than the combined value of all other transactions for that year.

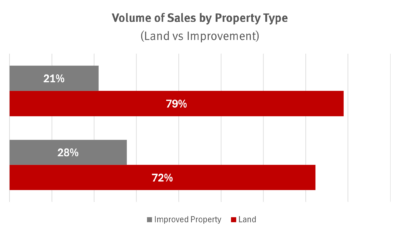

Sales Breakdown: Land vs. Improved Properties

• Vacant land continues to dominate the real estate market with 79% of the total volume of sales registered (289 land sales).

• Total number of land sales increased by 9% in 2025 Q1-Q2 when compared to 2024 Q1-Q2.

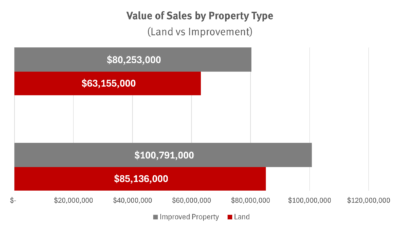

• Value of land sales is 44% of the total value of sales, and improved sales is 56% of the total value of sales.

Volume & Value of Transactions by Parish

- The top-performing parishes (St. George, St. Andrew, and St. David) have been consistent for several years.

- Approximately 81% of the total volume of sales was registered within St. George, St. Andrew, and St. David

- St. George accounted for 45% of the total volume of sales and approximately 73% of the total value of sales

- Although St. Andrew had greater volume of sale than St. David, the total value of sales in St. David was higher.

Overall market trends in the parishes remain consistent with real estate activity concentrated in St. George, the most populous parish with high demand for residential and commercial properties. St. Andrew continues to dominate agricultural sales, while Supply and demand continue to grow in the parish of St. David.

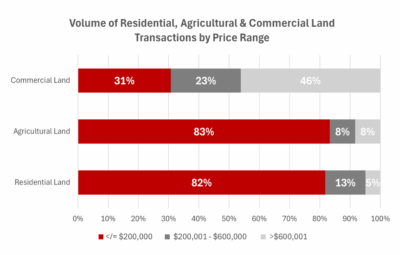

Sales by Price Range

Key Insights

Residential Land

- Up to EC $200,000: This price range dominated land sales, accounting for 82% of the total residential land transactions. These sales were primarily concentrated in St. George (36%), St. Andrew (29%), and St. David (17%).

- EC $200,001 – $600,000: This mid-range segment represented 13% of residential land sales, with St. George (66%) and St. David (23%) dominating.

- EC $600,001 and above: These land sales made up 5% of transactions. Land sales in “prime residential neighbourhoods” of Lance Aux Epines and True Blue contributed significantly.

Commercial Land

Commercial land sales were concentrated in the higher end of the price range (EC $600,001 and above), reflecting the premium value of commercial land. The data highlights the strong demand for commercial land in St. George. The 31% noted for commercial land sale on the lower price range were transactions of smaller lots used/purchased for commercial purposes.

Agricultural Land

Agricultural land sales are typically concentrated at the lower end of the price range, this has been the trend for several years and is expected to continue, these sales were predominantly in St. Andrew.

Sales by Property Classification: Residential, Commercial, and Agricultural

Residential sales have continued to dominate the market in Grenada, accounting for 92% of total sales volume and 79% of total sales value, reflecting strong demand for vacant land and residential homes. These transactions are primarily local buyers and buyers from the diaspora, with some participation from international markets.

Commercial sales, while representing a smaller share of the market, still played a significant role, contributing a substantial 19% of total sales value from a modest 5% of total sales volume. This highlights the high-value nature of commercial transactions, particularly in the parish of St. George, where demand for retail, office, and hospitality spaces remains robust.

Agricultural sales made up 3% of total sales volume and 2% of total sales value, indicating a low but steady interest in farmland and rural properties. This segment appeals primarily to local buyers.

Residential and commercial sales have been mostly concentrated in St. George, confirming the appeal for properties within this parish, as it hosts the largest segment of the population and desired amenities. However, St. Andrew continues to be the prevalent location for agricultural sales.

Conclusion

The Grenada real estate market presents a picture of steady, sustainable growth. We anticipate current market trends to continue into the foreseeable future, with growing interest in condominium developments and commercial real estate activities. It is expected that there will also be an increase in land development and affordable housing, both from the government and private developers.

The dominance of land sales points to future development potential, while the concentration of value in improved properties and commercial transactions underscores the maturity of key parishes. For investors and developers, the opportunity lies in understanding these segmented dynamics: targeting green fields for future land development in strategic locations, premium commercial developments in St. George, and recognizing the emerging value proposition in St. David. The market’s stability makes it a reliable environment for investment, with clear signals pointing towards strategic areas for future growth.