Market Overview

Demand is alive but selective. Terra Caribbean’s pipeline shows buyer introductions and showings both growing strongly year-on-year — serious buyers are active, but taking more time to commit.

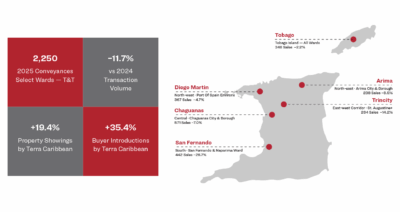

Registered residential sales activity across Trinidad & Tobago’s key corridors recorded 2,250 conveyances and lease assignments in

2025 — a reduction of 11.7% from 2024’s 2,549. These figures cover six select wards tracked by the land registry and do not represent

the full national market.

Market Overview & Key Indicators 2024 VS 2025

Demand Signal

Registered volume eased in 2025, but Terra Caribbeans’ proprietary pipeline tells a different story — buyer introductions and showings

both grew strongly (annually). The gap between activity and closed transactions reflects a more selective, patient buyer — not an absence of demand. Demand for $4M introductions has surged by 54% year-over-year.

Area Commentary

Diego Martin

Established western corridor. Volume near 2023 baseline. Demand underpinned by supply scarcity and an affordability sensitive buyer profile.

Trincity

East-west corridor — accessible entry price point. Moderation reflects sub-$1.5m affordability constraints, not structural confidence loss.

Arima

Activity broadly in line with 2024. Value proposition intact — affordable owner-occupier market with strong Churchill–Roosevelt Highway access.

Chaguanas

Chaguanas remains the highest-volume ward. Demand in the Central corridor stays strong as more homes, services and businesses continue to move out of Port of Spain.

San Fernando

Most notable contraction, though 2024. Return to 2023 levels suggests normalization, not decline. A new Hilton hotel and possible restart of the refinery may spur demand.

Tobago

Tobago’s property market remains sluggish. The ANR Robinson Airport upgrade and recently approved Marriott Hotel development signal growing investment confidence in the island as both a lifestyle and rental income destination.

Sales Trends — Six Select Wards

Construction Costs & Developer Outlook

Market Implications

The Replacement Cost Argument

A residential property costing TTD$1M to build in 2020 requires approximately TTD$1.3M in materials alone today — before labour or

professional fees. This creates a structural floor under well-positioned existing stock and makes new development difficult to justify at

current sales values. Slow approval process further exacerbates the issue.

TCL Cement — The Key Structural Driver

Six consecutive annual price increases since 2021. The most recent 15% rise (Feb 2026) was driven by NGC industrial gas price hikes

— structural, not temporary. T&T ranks 3rd highest in Caribbean for construction cost escalation (BCQS 2025), while achievable sales

values remain among the region’s lowest.

Developer Outlook

Margin Compression

Speculative residential development — particularly sub-$3m — is increasingly difficult to underwrite. Cement, electrical, and labour escalation must be priced in from inception.

Existing Stock Value

Rising cost support pricing of existing inventory relative to replacement cost. Buyers increasingly understand what building costs — and existing stock benefits.

Watch: Post-2022 Trend

Composite materials index averaged under 4% p.a. post-2022 — supply chains largely normalized. Cement and steel remain the structural outliers, driven by TCL pricing and global import costs respectively. Overall cost pressures have stabilized but the floor is higher than pre-2020.

The cost of building new acts as a price ceiling that never descends — it only rises. For buyers of existing stock, this is a structural argument for acquisition that goes beyond market timing.

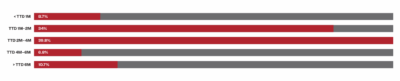

Price Band Distribution — TC 2025 Sales

Buyer & Seller Guidance

The Active Market

The TTD $1M–$4M band represents approximately 74% of 2025 sales. Most transactions occur between $1M – $2.5M. This is the engine of the market. Buyers and sellers in this range are operating in the most liquid segment and discounts are most limited.

2025 Discount Distribution Off Asking Price

Based On Terra Caribbean Closed Transactions 2025. | Discount = difference between asking price and achieved sale price.

For Buyers

A negotiated offer in the 5–15% range of asking is market-normal and well-supported by data. Buyers with pre-approved financing and a clean offer, without conditions, are in the strongest position. Motivated sellers are negotiating, but well-priced homes don’t wait.

For Sellers

Properties that arrive at market with a realistic asking price, transact faster and at better net outcomes than aspirationally priced listings. Time on market is money lost. Often the first offer is the best.

Negotiation Is Standard Practice In This Market

Negotiation is not a sign of distress, it is a part of the Trinidad & Tobago residential market. In 2025, the large majority of closed transactions involved some negotiation off the asking price, however, in early 2026 we have recorded several transactions at or over asking price.

We like questions, if you have one, or would like Brokerage, Valuation, or Marketing advice, we would love to hear from you!